|

| sky falling

Who is afraid of TRID?

Will it delay my closing?

The answer is NO for just about everybody.

When the Know Before You Owe mortgage disclosure rule becomes

effective, lenders must

give you the new, easy to read disclosures about your loan three

business days before closing.

Think of it as a lemon law to check and review

before the last minute.

This gives you time to review the terms of the deal before you

get to the closing table.

Many things can change in the days leading up to closing. Most

changes will not require

your lender to give you three more business days to review the

new terms before closing.

The new rule allows for ordinary changes that do not alter the

basic terms of the deal.

Only THREE changes require a new 3–day

review:

1. The APR (annual

percentage rate) increases by

1/4 of a percent for adjustable loans.1

A decrease in APR will not require a new 3-day review if it is

based on changes to interest rate or other fees.

2. A prepayment penalty is

added, making it expensive to

get out of the mortgage to sell or refinance lower.

3. The basic loan product

changes,

Such changing from a thirty year fixed rate to adjustable rate

or say a fixed to an interest only.

These would be big changes to the loan long

term.

1 Lenders have been

required to provide a 3-day

review for these changes in APR since 2009.

NO OTHER changes require

a new 3–day review:

There has been much misinformation and mistaken

commentary around this point. Any other changes

in the days leading up to closing do not require a

new 3-day review, although the lender will still have

to provide an updated disclosure.

Sometimes Chicken Little Yelling that the Sky is Falling

requires cool heads, planning, organization and not a

foil chicken helmet

The following situations do not require a new 3-day review:

Unexpected discoveries on a walk-through

such as a broken refrigerator or a missing stove,

even if they require seller credits to the buyer if nominal.

Most changes to payments made at closing,

including the amount of the real estate Commissions, taxes,

pro-rations for utilities and amounts paid into escrow impounds.

Typos found at the closing table.

Spelling errors, okay that's pretty common sense

|

7/23/2015

Sky Falling TRID Coming?

7/17/2015

Call me to get on the MLS

|

7/12/2015

Open House 25 White Sail

My first open house (well not the maiden voyage of holding an open house as I have done hundreds) but this one is special.

Okay here is my list of done items

Boxed up photographs of my children, myself and our adventures

Jewelry in safe deposit box

Tossed safely all extra and old medicines

Guns in safe deposit box (perhaps not politically correct but this girl yes)

Wine cellar emptied

Painted everything excepting daughter's room which I think I'm going to have someone do it-

not enough time for getting her giant mural down and the Ives Klein Blue is going to be a triple coat

Garage sales cleaned out about half of the treasures in the garage, need to sell the rest on ebay

(Anyone need extra surf boards, weight equipment, a treadmill, artwork, mister system and a huge variety of women's designer clothing I purchased in the flush years before the crash that daughter never wore- let me know)

Every thing from window screens, under sinks, tubs, and windows is super clean.

Threw away some area rugs, donated others

Pool is clean fountain running but the dang trees will surely drop stuff all day for me

Cut down the pigmy palm that blocked south side ocean view (yes I used a chain saw)

cleaned glass wall to sparkle up the ocean and canyons views.

Trimmed down all my sweet peas and harvested seeds ( a little early but they were leggy and messy looking)

Power washed brick and driveway

Steaming rosemary, lemon peels and vanilla for air perker freshener smell "betterer" (it's better than fabreze or candles or cookies)

Dog bowls in laundry room, Honey had a bath but she will go to grandma's for the afternoon. Honey is almost 14 out Golden Retriever who is deaf and sunbathes but would greet everyone with fluffy hair.

all laundry washed dried and put away

Kitchen sink looks super white brand new

Did I say I dusted, scrubbed and cleaned again last night?

What did I miss?

Took down the rosary and cross above my dresser.

Hope the kids don't come home and start cooking a nice curry dish at 2:00.

How do I lure buyers to stay out backyard and me romanced by the view, the hummingbirds, the Bells Vireo who is nesting in the gazebo?

1:00 - 4:00

July 25 and July 26th

Saturday and Sunday

come on by

25 White Sail Laguna Niguel

Free organic tomatoes and herbs for the visit!

For Sale By Owner

$1,659,000.00

4 bedrooms 3410 square feet 2 story Cape Code style board and batten singles More than one hundred varieties of roses, organic vegetable gardens, pool, spa, huge party barbecue,

Did I say OCEAN Views from many rooms?

Downstairs bedroom and full bath

Could be 5 bedrooms if you make the huge bonus room have a small closet

(949) 784- 9699

3 fireplaces, plus outdoor fire pit and heater

barbecue with sink, tiled counters, and brick storage areas

brick seating and planters

Two gazebos

Hardwood floors in six in plank downstairs

San Marin Homeowner Association

Okay here is my list of done items

Boxed up photographs of my children, myself and our adventures

Jewelry in safe deposit box

Tossed safely all extra and old medicines

Guns in safe deposit box (perhaps not politically correct but this girl yes)

Wine cellar emptied

Painted everything excepting daughter's room which I think I'm going to have someone do it-

not enough time for getting her giant mural down and the Ives Klein Blue is going to be a triple coat

Garage sales cleaned out about half of the treasures in the garage, need to sell the rest on ebay

(Anyone need extra surf boards, weight equipment, a treadmill, artwork, mister system and a huge variety of women's designer clothing I purchased in the flush years before the crash that daughter never wore- let me know)

Every thing from window screens, under sinks, tubs, and windows is super clean.

Threw away some area rugs, donated others

Pool is clean fountain running but the dang trees will surely drop stuff all day for me

Cut down the pigmy palm that blocked south side ocean view (yes I used a chain saw)

cleaned glass wall to sparkle up the ocean and canyons views.

Trimmed down all my sweet peas and harvested seeds ( a little early but they were leggy and messy looking)

Power washed brick and driveway

Steaming rosemary, lemon peels and vanilla for air perker freshener smell "betterer" (it's better than fabreze or candles or cookies)

Dog bowls in laundry room, Honey had a bath but she will go to grandma's for the afternoon. Honey is almost 14 out Golden Retriever who is deaf and sunbathes but would greet everyone with fluffy hair.

all laundry washed dried and put away

Kitchen sink looks super white brand new

Did I say I dusted, scrubbed and cleaned again last night?

What did I miss?

Took down the rosary and cross above my dresser.

Hope the kids don't come home and start cooking a nice curry dish at 2:00.

How do I lure buyers to stay out backyard and me romanced by the view, the hummingbirds, the Bells Vireo who is nesting in the gazebo?

1:00 - 4:00

July 25 and July 26th

Saturday and Sunday

come on by

25 White Sail Laguna Niguel

Free organic tomatoes and herbs for the visit!

For Sale By Owner

$1,659,000.00

4 bedrooms 3410 square feet 2 story Cape Code style board and batten singles More than one hundred varieties of roses, organic vegetable gardens, pool, spa, huge party barbecue,

Did I say OCEAN Views from many rooms?

Downstairs bedroom and full bath

Could be 5 bedrooms if you make the huge bonus room have a small closet

(949) 784- 9699

3 fireplaces, plus outdoor fire pit and heater

barbecue with sink, tiled counters, and brick storage areas

brick seating and planters

Two gazebos

Hardwood floors in six in plank downstairs

San Marin Homeowner Association

7/07/2015

TRID Mortgage Rules

Don't forget to email your dog license.

In review the new CFBP TILA - RESPA Integrated Disclosures

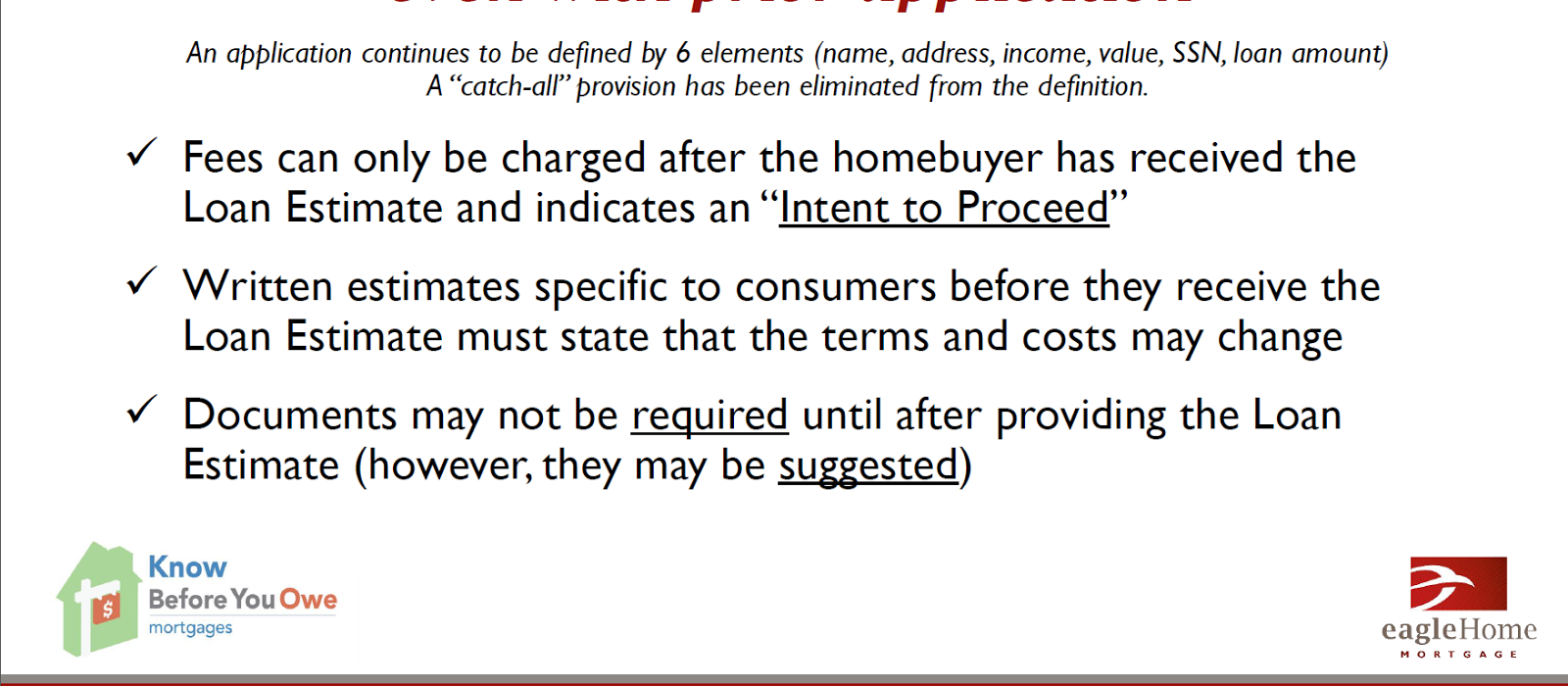

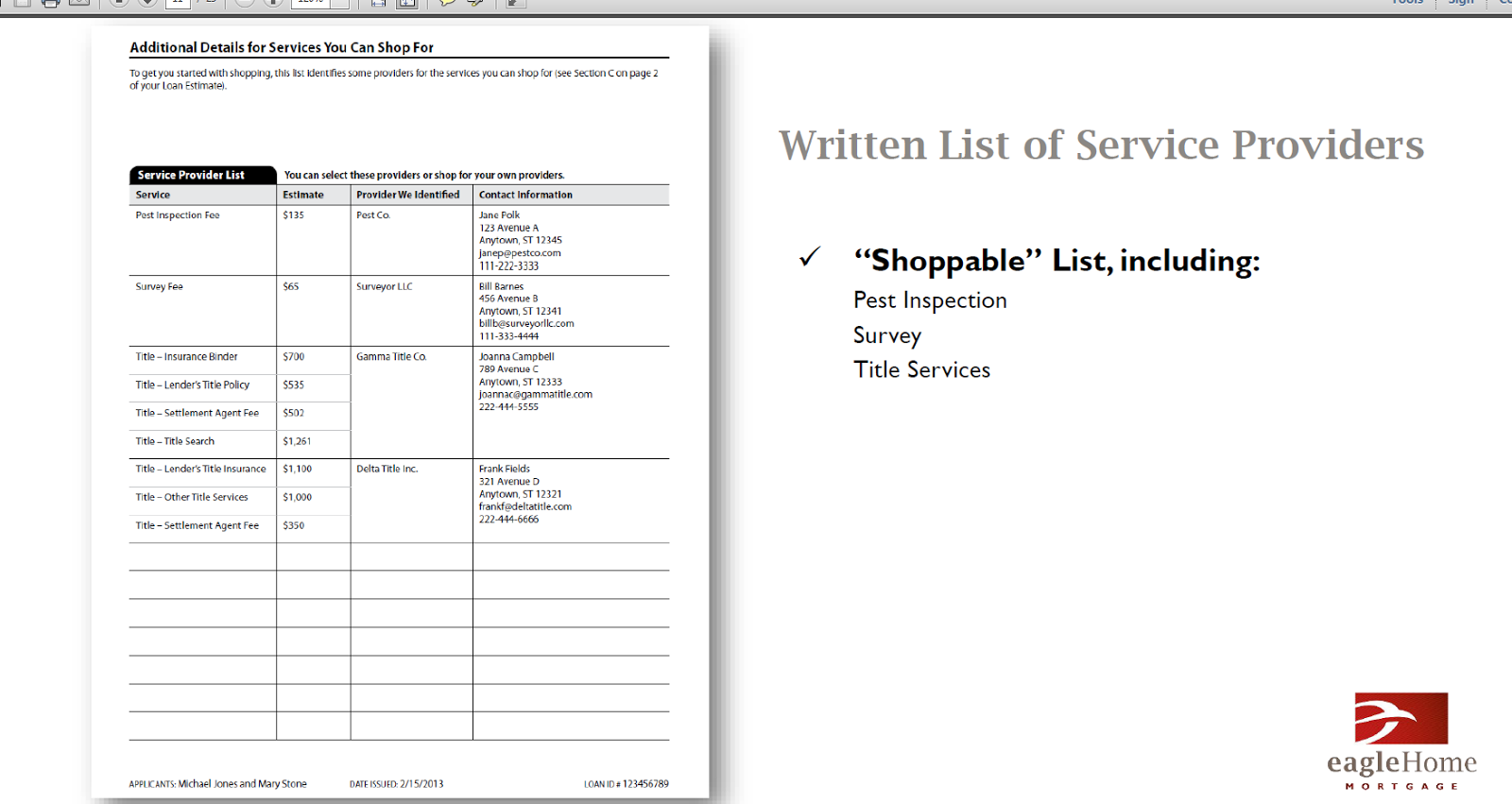

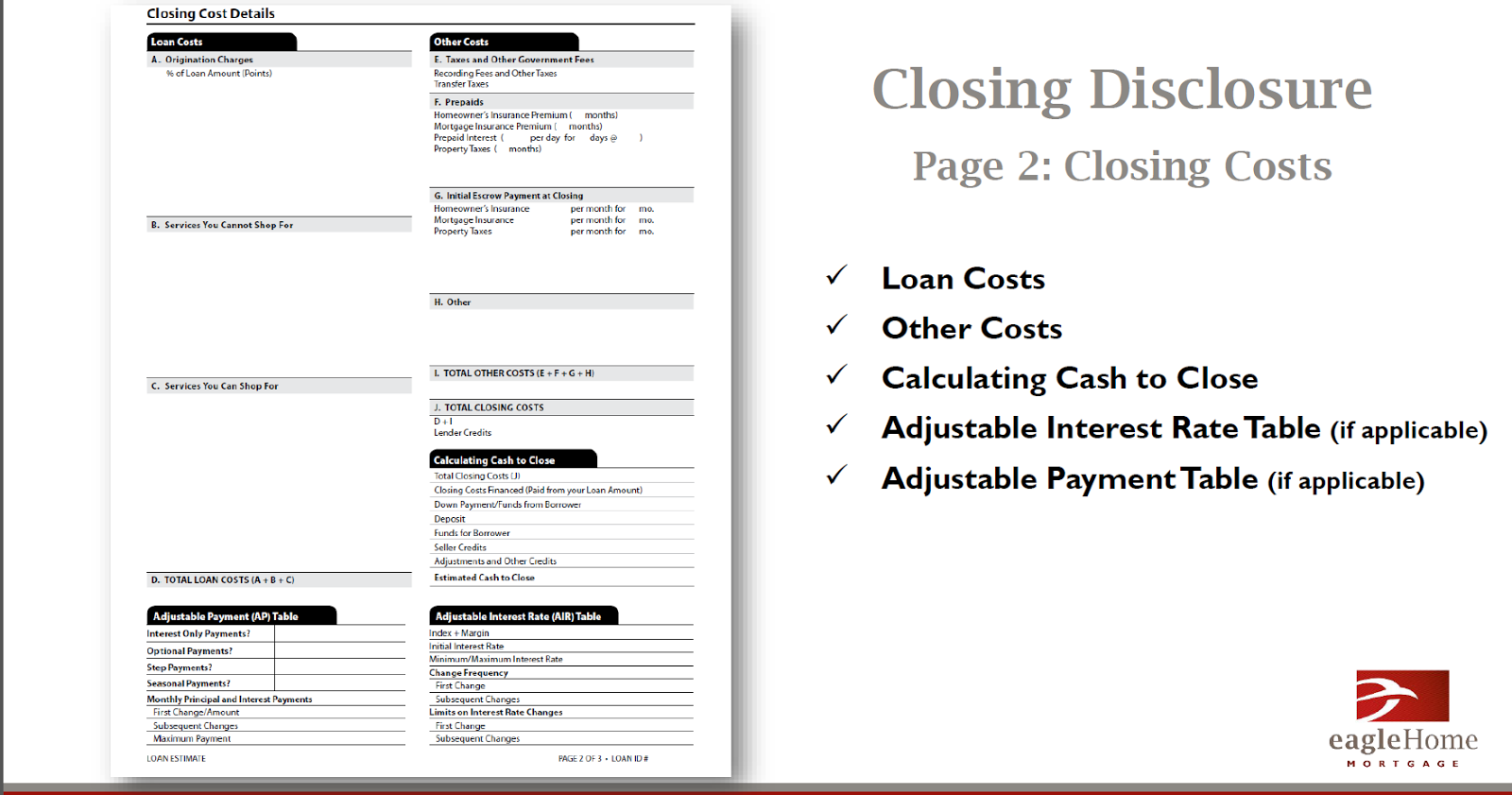

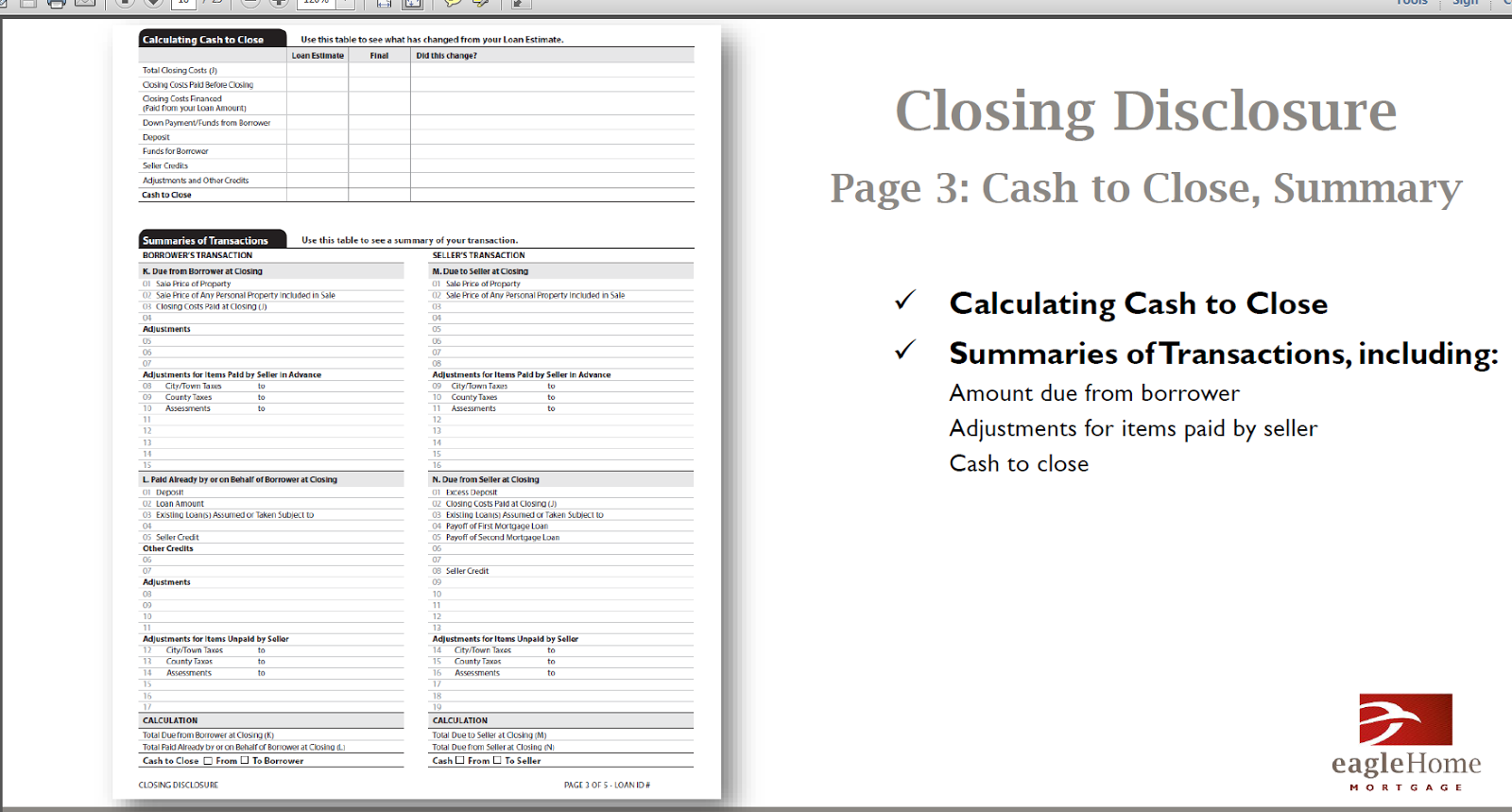

TRID adds a "lemon law" like disclosure at closing more strict than what was in place for refinance owner occupied mortgages. Now the forms TIL and Good Faith are simplified but No room for escrow or attorney nationwide to make estimate errors. All costs have to be right on the money.

This means Realtors can no longer add credits, rebates, seller credits for repairs or termite or softening credits to make buyers close on the last days. This would add additional wait days, require appraisers to review the value and buyers to wait. Rate locks may need to be extended accordingly.

New law that is pretty easy to follow but perhaps not so great for consumers. Added wait times is now what buyers borrowers and real estate agents want.

Here at Eagle and Universal Home Mortgage we are already working to implement these changes.

Educating Realtors to make money credit agreements upfront or to avoid last minute changes that will add days to a transaction.

It takes away my ability to offer cheaper 15 day rate locks as there may not be time to close and re-disclose if any numbers change, and they often do.

I can still close a loan in 30 days, or less.

copyright 2015 Caroline Gerardo Barbeau NMLS 324982

Subscribe to:

Posts (Atom)